Understanding the DBS Multiplier Account in 2020 - It May Not Be as Good as You Think and Bonus Interest Rates Will Be Reduced on 01 May 2020

The DBS Multiplier Account allows you to earn higher interest rates of up to 3.8% p.a. on savings up to S$100,000. To even consider this account, you will need to receive some kind of monthly income (either through the form of Salary or Dividends) and your monthly total eligible transactions (I'll explain more on this later!) need to add up to at least S$2,000.

Photo Credit: DBS

Firstly, I personally dislike it when banks advertise an interest rate that is higher than what the Effective Annual Rate (EAR) is. Now DBS advertises a bonus interest rate of up to 3.8% p.a. (which is not incorrect) but even in the best-case scenario (i.e. if you are able to fulfill the highest requirements needed to trigger the most bonus interest), the EAR is only 3.65% p.a.. Confused? Let's understand how the DBS Multiplier Account works first.

Photo Credit: DBS

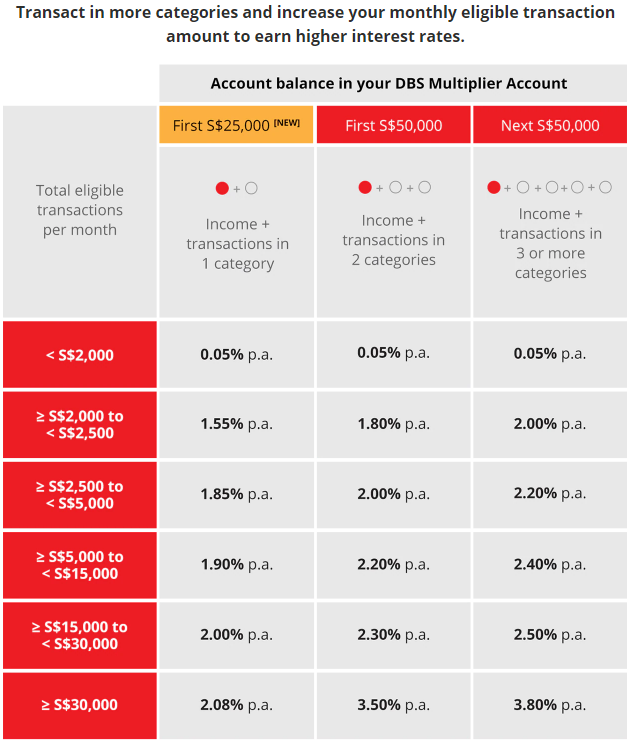

Everything you need to know about the DBS Multiplier Account revolves around the table above. The amount of bonus interest that you can earn on this account is dependent on two things - Monthly Total Eligible Transactions and Account Balance.

You'll Need to Credit Your Income (Salary/Dividends) into a Deposit Account

As mentioned earlier, to even benefit from the higher interest rates, you will have to credit your income (from salary and/or dividends) into the account each month. If you are crediting your monthly salary, the DBS Multiplier Account requires it to come through in a particular way:

Salary must be credited via GIRO, with transaction reference code 'SAL' or 'PAY'. This is reflected as either 'GIRO SALARY' or 'SALARY' in the main transaction description in your Statement of Account.

If you are crediting your dividends in your DBS or POSB deposit account, this is what you need to know in order to be eligible for the bonus interest rates:

Dividends must be credited via GIRO, from Central Depository Pte Ltd (CDP) with transaction reference codes ‘CDP’ or ‘NDIV’. For customers with DBS Wealth Management Account: Dividends must be credited from Singapore Exchange (SGX) traded securities.

As a quick reminder, there is no longer a minimum income requirement for the DBS Multiplier Account each month. The total income that comes into your account goes towards the calculation of your monthly total eligible transactions.

Photo Credit: DBS

You'll Need to Transact in One or More Categories

Apart from crediting your income (which may come from your salary or dividends), you will have to transact in at least one of four categories set-out by the DBS Multiplier Account. As you can imagine, transacting in more categories will allow you to enjoy a higher interest rate on your total account balance (up to S$100,000). There are four main categories under the DBS Multiplier Account and there is no minimum amount required within each one of them (but the total eligible transaction amount needs to add up to at least S$2,000 each month):

Credit Card Spend - total eligible spend across main and supplementary cards

Home Loan Instalments - monthly instalment due (both cash and CPF are included)

Insurance - regular premium policies purchased after opening the Multiplier Account

Investments - new DBS Invest-Saver, unit trust lump-sum contribution or trade in equities online via DBS

Do check out the 'More Information' section of the DBS Multiplier Account page if you need additional information on each one of the aforementioned categories but it should be fairly straightforward.

You'll Need to Transact at Least S$2,000 Each Month Across Categories

As mentioned above, there are four main categories that you will have to transact in, and the total eligible transaction amount (including your income) needs to add up to at least S$2,000 each month. There are different bands of transactions and in order to trigger the most bonus interest on your DBS Multiplier Account, you will have to transact at least S$30,000 or more per month (which is rather difficult for an average consumer).

Photo Credit: DBS

Bonus Interest on Account Balance is Dependent on Transaction Categories

So you have learned how to navigate the bonus interest matrix which is at the top of this page - you earn the highest interest rates on the DBS Multiplier Account if you transact a lot across at least 3 categories. However, you should take note that the account balance in which the bonus interest is applicable, is dependent too on the number of categories that you transact in. Essentially, you will only earn the published bonus interest rates on the following account balances:

Transact in 1 Category: S$25,000

Transact in 2 Categories: S$50,000

Transact in 3-4 Categories: S$100,000

To put this into a simple example, let's assume that you have S$100,000 savings in your DBS Multiplier Account and you receive a salary of S$3,000 (after CPF contributions) each month. On top of that, you also spend S$1,000 on your DBS Woman's World Mastercard because it gives you 4 miles per dollar on all eligible online spending. Now your monthly total eligible transactions add up to S$4,000 this month and that puts you in the second band of the bonus interest rates. However, since you have only transacted in one category (credit card spend), you will only earn 1.85% p.a. bonus interest (or 1.60% p.a. from 01 May 2020) on the first S$25,000 of your S$100,000 balance - the other S$75,000 will earn a miserable 0.05% p.a. and this means you are earning an EAR of 0.5% p.a. on your S$100,000 balance (uh-huh).

Regardless of how much you have in your Multiplier Account, you will only earn a bonus interest of up to 3.80% p.a. (or an EAR of 3.65% p.a.) if you transact across three or four categories each month! There is a really handy feature on the DBS page which allows you to 'Calculate Your Savings' and I highly recommend that you do that before making any decision to switch (or sign-up!).

Photo Credit: DBS

Bonus Interest to be Reduced from 01 May 2020

Now if you are the kind that will only transact in only one out of four categories, you should seriously consider a different product - I personally like the OCBC 360 Account a lot better. Now if for some reason, you have worked out the math and you still think you are in a great position with the DBS Multiplier Account (despite transacting only in one category each month), the bonus interest rates will be reduced on the first S$25,000 of your total account balance from 01 May 2020.

Final Thoughts

I am not saying that the DBS Multiplier Account (despite transacting only in one category each month) is a bad product. If you are the kind that transacts quite a bit each month across multiple categories, you can potentially get up to S$3,650 of interest per year on the first S$100,000 (EAR of 3.65%) in your account. However, if you are drawn to the 3.8% p.a. interest that DBS advertises, you should definitely work out what your estimated 'savings' would be - something tells me that it will be a lot lower than what you have initially expected.

HSBC is removing the 1% p.a. Everyday+ bonus interest on the Everyday Global Account from 1 July 2026, cutting the headline stacked rate by a full percentage point. Here is what it means for your savings strategy.