Revisions to OCBC 360 Account Bonus Interest Rates From 02 May 2020 - Should You Continue to Put Your Savings Here?

There are quite a number of saving accounts out there that will allow you to enjoy bonus interest rates if you credit your monthly salary into them. In view of the business environment right now, many banks are making changes to their existing products in order for them to remain competitive in the market. Last night, I received an EDM on the upcoming changes to the OCBC 360 Account on 02 May 2020 and while I have actually braced myself for the worst, it is actually not all that bad.

Photo Credit: OCBC

Coincidentally, I wrote about the DBS Multiplier Account yesterday and I penned down some of my thoughts surrounding that product. What I do like about the OCBC 360 Account (and it is the one that I actually use) is clarity - it does not hide behind complicated mechanics and it advertises the product in a way that does not mislead an average consumer. OCBC 360 Account holders are currently able to earn an effective annual rate (EAR) of up to 3.45% p.a. on the first S$70,000 in their account but with the upcoming changes that will go live on 02 May 2020, the EAR will be reduced to 3.35% p.a..

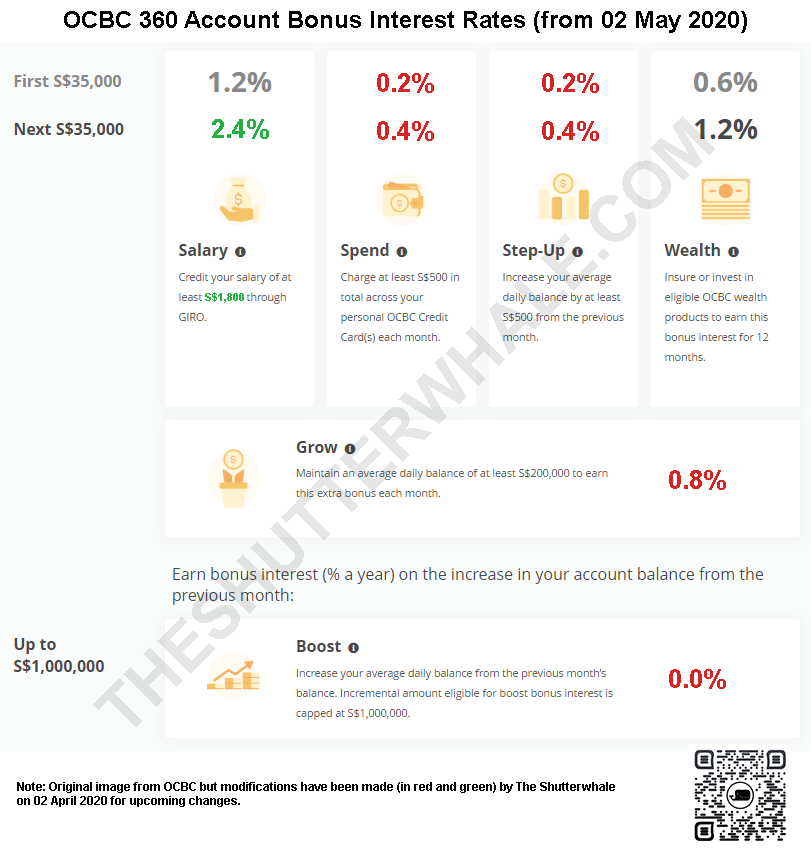

Effective Until 01 May 2020 | Photo Credit: OCBC

Lower Minimum Salary Requirement (from S$2,000 to S$1,800)

One of the basic requirements of the OCBC 360 Account is to credit a monthly salary of at least S$2,000 through GIRO. On 02 May 2020, the minimum salary requirement will be reduced to S$1,800 to make it slightly more accessible to an average Singapore resident (especially those who have just started to work).

Changes to Bonus Interest Rate

While the entire account balance of the OCBC 360 Account earns a base interest rate of 0.05% p.a., you can get up to 3.45% p.a. on the first S$70,000 in your account if you satisfy four different criteria:

Salary

Spend

Step-up

Wealth

As mentioned earlier, account holders can earn a bonus EAR of up to 3.45% p.a. right now on the first S$70,000 in the OCBC 360 Account. Starting from 02 May 2020, the EAR will be adjusted down to 3.35% p.a. which is obviously not ideal but the changes are in fact quite negligible - S$5.83 less interest per month. I will not explain the mechanics of the OCBC 360 Account again in this article since it is pretty straightforward and I have covered it previously.

Effective from 02 May 2020 | Photo Credit: OCBC

I. Increase in Salary Bonus (EAR from 1.60% p.a. to 1.80% p.a.)

The OCBC 360 Account offers two tiers of bonus interest - a lower bonus interest rate applies to the first S$35,000 and a higher one applies to the next S$35,000. Starting from 02 May 2020, the bonus interest rate on the second S$35,000 will increase from 2.00% p.a. to 2.40% p.a. - this brings the entire EAR of the Salary Bonus from 1.60% p.a. to 1.80% p.a.. Effectively, if you meet the minimum salary requirement for the account, your effective interest from this category will increase from S$1,120 to S$1,260 (S$140 more!) per year assuming a S$70,000 account balance.

II. Decrease in Spend and Step-up Bonus (EAR from 0.45% p.a. to 0.30% p.a.)

Unfortunately, OCBC will be introducing some negative changes to the OCBC 360 Account - the bonus interest rates on the Spend and Step-up categories will decrease from 0.30%/0.60% for the first/second S$35,000 blocks to 0.20%/0.40% - this brings the EAR for both categories down from 0.45% p.a. to 0.30% p.a.. If you have a S$70,000 account balance, your bonus interests from these two categories will reduce from S$630 to S$420 (S$210 less!) per year. If you are looking for an OCBC credit card to spend on, the OCBC Titanium Rewards Card is a great card to have since it gives you 4 miles per dollar on eligible transactions (capped at S$12,000 each membership year) - new-to-card customers can also get S$100 cash reward if they sign-up now!

III. No Change to Wealth Bonus (EAR at 0.90% p.a.)

The Wealth Bonus of the OCBC 360 Account requires you to insure or invest in eligible OCBC wealth products for 12 months. I could be wrong but I do not think most of the OCBC 360 account holders actually utilise this category. In any case, there will be no changes to the Wealth Bonus - you will still earn 0.60% p.a. and 1.20% p.a. for the first and second S$35,000 blocks in your OCBC 360 Account respectively.

IV. Decrease in Grow Bonus (EAR from 1.00% p.a. to 0.80% p.a.)

The OCBC 360 Account currently rewards you with a Grow Bonus - you will need to maintain an average daily balance of at least S$200,000 to earn this extra bonus each month. Once again, I do not think most of the OCBC 360 Account holders actually fall into this category (especially since S$200,000 AUM with OCBC gives you access to Premier Banking and I personally think you can do better things with money than just having it sit in a savings account). The Grow Bonus will decrease from 1.00% p.a. to 0.80% p.a. from 02 May 2020.

V. No More Boost Bonus (EAR from 1.00% p.a. to 0.00% p.a.)

The OCBC 360 Account currently gives you a Boost Bonus Interest of 1.00% p.a. if you increase your average daily balance from the previous month’s balance but there will no longer be a Boost Bonus from 02 May 2020. The incremental amount eligible for boost bonus interest is currently capped at S$1,000,000 and there were many ways to creatively take advantage of this previously but this benefit will be removed next month.

Final Thoughts

While there will be some positive and negative changes to the OCBC 360 Account on 02 May 2020, and we will end up with a lower EAR of 3.35% p.a. (instead of the current 3.45% p.a.), I guess it is safe to say that the changes are actually not that bad. When you think about the current business landscape (no doubt made worst by the spread of the COVID-19 pandemic worldwide), I think that the upcoming changes are reasonable (especially when you consider what competing banks are doing). I would personally still maintain a balance of S$70,000 in the OCBC 360 Account (but nothing more) personally and think about putting the rest of money towards getting a higher rate of return with riskier assets.

HSBC is removing the 1% p.a. Everyday+ bonus interest on the Everyday Global Account from 1 July 2026, cutting the headline stacked rate by a full percentage point. Here is what it means for your savings strategy.